Tangerine Investment Funds Review

Tangerine Bank is known for having one of the best high interest savings accounts in Canada, but they also offer Tangerine index funds. This product is an easy way to get you investing while minimizing the fees you’ll pay.

Admittedly, Tangerine investment funds are more expensive compared to robo advisors or ETFs, but I still think they’re a great product. Keep reading my Tangerine investment funds review and find out why they may be a good fit for you.

What are index funds?

Index funds are funds where its holdings are meant to match a certain market index. Since an index comprises of the stock of thousands of companies, it allows an investor to be well diversified. There are many different indexes, but the Tangerine investment funds try to mimic the following indexes.

- FTSE TMX Canada Universe Bond Index – Canadian Bonds

- S&P/TSX 60 Index – Canadian Stocks

- S&P 500 Index – US Stocks

- MSCI EAFE (Europe, Australasia and Far East) Index – International Stocks

Don’t worry if you didn’t understand a word of the above, all you need to know is that index investing allows you to own the entire market as opposed to individual stocks. This benefits you as an investor since it has been proven that 80% of the time active management doesn’t beat the indexes.

It’s true that 20% of the time mutual funds do beat the index, but there’s no guarantee that you’ll be invested in the right fund. Plus past performance is not an indicator of future outcomes. Some investment advisors claim that their active style will guarantee returns or prevent any losses, but in reality, no one can predict the future.

Becoming an index investor over the years has become quite popular since people are starting to understand how fees can eat at your returns over time. For reference, all of Tangerine’s investment funds have a management expense ratio (MER) of 1.07%, whereas mutual funds charge an average MER of 2.5%. That’s a huge saving over your investment lifetime. Like tens if not hundreds of thousands of dollars.

There are five diversified portfolios available to investors with Tangerinewhich range from safe to risky. To find out which portfolio is right for you, you’ll be asked a series of questions to determine your investor profile before a recommendation is made. If you’re curious about how they all stack up, here’s my Tangerine investment funds review.

Tangerine Balanced Income Portfolio

- Fund code: INI210

- MER: 1.07%

- Risk Factor: Low

Of all the investment funds available from Tangerine, the Balanced Income Fund is the safest for investors since it has 70% in bonds. There is still some minor growth potential since 30% of your portfolio is invested in equities but this fund is aimed at people who aren’t looking for many risks.

New investors who may not be knowledgeable might lean towards a safe portfolio, but if you’re young, you really should be using a portfolio that has a higher allocation towards stocks. Even if the markets drop, you’ll have plenty of time to recover.

Tangerine Balanced Portfolio

- Fund code: INI220

- MER: 1.07%

- Risk Factor: Low – Moderate

As the name implies, the Balanced portfolio offers a balance between fixed income and equities. This will allow your portfolio to grow while still maintaining stability.

Traditionally, this portfolio would appeal to people who are in their 40’s as one rule of thumb is that the bonds in your portfolio should match your age. However, since people are living longer, and you could still be investing for 20+ years when you retire, this asset allocation is becoming a more popular choice for people in their 50’s or 60’s.

Tangerine Balanced Growth Portfolio

- Fund code: INI230

- MER: 1.07%

- Risk Factor: Moderate

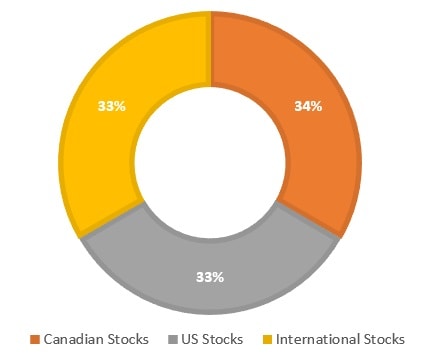

With an even allocation between Canadian bonds, Canadian stocks, U.S. stocks, and International stocks, this is the perfect portfolio for investors in their 20’s and 30’s. You’re getting a lot of exposure to stocks so there’s a lot of potential for growth. This portfolio also has an equity allocation spread around the world so there’s no home base bias.

Tangerine Equity Growth Portfolio

- Fund code: INI240

- MER: 1.07%

- Risk Factor: Risky

This is Tangerine’s riskiest fund. There are no bonds to balance the fund out during down markets. Risky might be a loose term as it still makes sense for a lot of people.

Someone in their 20’s who has 40+ years to invest will likely have no problem starting with this portfolio. Alternatively, if you have a pension plan from work or you want to take a more aggressive approach in your TFSA, this portfolio could be a good choice.

Tangerine Dividend Portfolio

- Fund code: INI235

- MER: 1.07%

- Risk Factor: N/A

This is Tangerine’s ‘newest’ fund. It started in late November of 2016, so it doesn’t have much history. However, it tracks the MSCI Canada High Dividend Yield Index, the MSCI USA High Dividend Yield Index, and the MSCI EAFE High Dividend Yield Index which have been around for a while.

If you’re looking for a dividend paying Tangerine fund, this is the one for you. Distributions are paid out annually in December.

Tangerine investment funds review

PROS

- Low Management Expense Ratio (MER)

- No account or trading fees

- No minimum investment required.

- Auto Rebalancing

CONS

- Not the cheapest option (MER)

- Limited to 5 Investments funds

- Unable to modify asset allocation

The Tangerine investment funds are attractive to new investors since all you need to do is deposit your money and Tangerine will take care of everything. You can also set up an automatic saving plan with the funds, so you can just set it and forget it. There are no additional fees and you can purchase the Tangerine investment funds in your RRSP, TFSA, and regular account.

The recent change to the equity growth fund and the addition of the dividend portfolio has addressed the concerns of investors. All things considered, the 1.07% MER is reasonable for people who want to index without becoming a do-it-yourself investor.

How do Tangerine investment funds compare to others

If you invest on your own and use the Couch potato strategy, you could easily bring your MER down to .2% using ETFs or .5% with TD e-Series funds. These options require a little more work, but you get complete control over your asset allocation. You may end up paying trading and account fees, but the overall lower MER still make it worth your while. Basically, you could replicate the Tangerine investment funds at a fraction of the cost.

For many people, investing their own money is not something they’re interested in at all. Fortunately, robo advisors are a good option. Many of the top robo advisors in Canada including Justwealth, Wealthsimple, WealthBar (now CI Direct Investing), Nest Wealth and RBC InvestEase charge fees in the .50 -.90 range so if you invest with them, you could save a bit more on your MER. In addition, most of those robo advisors have a special promo where you can some of your portfolio managed for free when using my referral link.

If robo advisors are cheaper, then why do people use Tangerine investment funds? Well, since Tangerine is owned by Scotiabank, many people prefer to use them. They like to know that their money is with a major Canadian bank. The other obvious comparison is the new Tangerine ETFs which are Tangerine’s version of all-in-one ETFs.

I personally don’t think it matters if you DIY, use a robo advisor or Tangerine investment funds. They’re all good options since the fees you pay will be much lower than traditional mutual funds.

Final thoughts

All things considered, my Tangerine investment funds review is positive. If you’re looking for an easy way to invest but are not confident in becoming a DIY investor, then the Tangerine funds are a very good option. If you have an interest in investing and prefer a little more control over then go with TD e-Series, Questrade, or robo-advisors.

Remember you could always start with Tangerine and then switch later, the point is to start investing early and avoid high-cost mutual funds. If you want to start investing in the Tangerine investment funds, use my referral to open an account and start saving now. Even if you decide to go with a different company for your investments, don’t forget that Tangerine has one of the best rates for high interest savings accounts in Canada.

Interesting set of funds, for those that don’t want the “Seat of your pants” feel of the raw index funds, might be a better option than the higher MER (> 2%) active management funds offered by others.

bigcajunman,

These funds are definitely valuable to certain type of investors. I used to use them myself before I switched to DIY investments.

what platform do you use for your DYI in Canada?

I loved the Tangerine funds. Even though I have a discount brokerage account, I still put my money away to my Tangerine funds automatically with my pay cheque.

Kat,

Yes they’re great funds that suit a variety of investors.

You say: I still put my money away to my Tangerine funds automatically with my pay cheque.

Sorry, how do you do this? Do you send physical checks? Where?

Julia,

I use TD Direct Investing to manage my portfolio. As for Tangerine automatic withdrawals to their investment funds, you can set it to withdraw from any account. That could be your Tangerine account or another bank account outside of Tangerine.

Barry, I am new to TD WebBroker. I don’t see the Tangerine mutual funds coming up when I search for them, or in any of the comparisons. Since you use TD Direct Investing, you might know what I am missing. I don’ t want to assume that TD is censoring investments.

I can find Tangerine in Morningstar independently of the TD platform.

Thanks in advance.

Hi Lonnie,

Tangerine investment funds are only available to Tangerine customers. To replicate them you can purchase VBAL, VGRO or VEQT. Alternatively, you could purchase TD’s e-Series funds if you plan on making monthly contributions.

Here are a few resources

https://canadiancouchpotato.com/

https://www.vanguardcanada.ca/individual/etfs/about-our-asset-allocation-etfs.htm

https://boomerandecho.com/vanguard-all-equity-etf-veqt/

Thanks, Barry. I AM a Tangerine customer but was hoping to research / compare Tangerine funds with other similar funds using WebBroker. I can do that on Morningstar but would rather do my research all in one place. It sounds like TD WebBroker only shows funds a person can actively buy from the platform. Would that be correct?

Lonnie,

That’s correct.

Canadiancouchpotato has a good breakdown of different model portfolios if you’re looking for examples. I don’t think they talk about past returns though.

All of the funds are similar. If you know what you’re doing, go with Vanguard since it’s the cheapest option. I personally started with Tangerine index funds, then went to TD E-series funds and now use Vanguard all-in-one ETFs.

Hi. Does Tangerine pay you or incent you in any way to review their funds? I don’t see any disclosure on your site.

Bee,

Any post that is sponsored I clearly disclose. In this specific case, no payment was made nor was I asked by Tangerine to review the funds. I just gave my honest assessment of the funds, you’ll notice that I state that there are other options (and cheaper) available to investors. But these funds are good for some people.

You are so right! I love Tangerine and will stick with them…after all they were the first to bring in the option of a much lower mer fee for all to choose.

Bee, yes, he will get money if you use his tangerine key (what the author calls “referral links”, and set up an account with tangerine, he will receive money (I believe its $50 per each new client paid to the existing client).

Think you forgot to put a period where it says “All things considered, the 107% MER …”

Oops!

Min Min,

Good catch! 1.07% is much more reasonable compared to 107%!

Hi Barry, I hope you can do a post on how to switch from another institution to Tangerine.

Thanks!

Hi Virna,

I believe if you already have accounts set up with Tangerine, you just need to contact them and fill out a form. They’ll initiate the transfer for you directly but you may have to pay a fee from your previous bank.

No performance?

Hai Sung,

Performance for each fund is listed on their website but remember past performance is not an indicator of future outcomes.

Interesting read.

I think you may have helped me with regards to whether I Should go with QTrade or Tangerine. I don’t do any trading myself, I don’t really understand it. I m retired and just want to use some of my savings to make money for future needs. I think I will go with Tangerine again. I have investment there all ready so I will just add to it.

As I have a small amount I fear investing with Q-Trade, my money will get eaten up.

Any thoughts?

Hi lYnn,

To me, it sounds like you need a little extra hand-holding so I would recommend using a robo-advisor. Despite the name, it’s not a robot who manages your portfolio, it would be a live person who passively helps you with your portfolio. They’ll be able to come up with a plan that fits your profile.

Off the top of my head, the ones I would look at include NestWealth, and WealthSimple. Both have reasonable fees (very close to what Tangerine charges)

Is 1.07% really a low MER? I’m just learning about low-cost index funds and it seems like other financial institutions have much lower MERs – but is that because they charge additional feeds on top of the MER? Thanks.

*fees, not feeds

Hey Erin,

Fair points. The 1.07% MER is the lowest from a “managed” mutual fund perspective. There are cheaper options such as robo-advisors, but Tangerine is still cheaper than your standard bank mutual fund MER which is about 2.5%.

However, if you were to manage things yourself with ETFs or TD e-series funds, your MER would drop below .50%. But that requires you to manage the funds on your own.

Tangerine funds are appealing because it’s a “name brand” even though they track the index which requires ZERO effort on your end.

I personally started with Tangerine funds, but then switched to ETFs. Note that when I started investing robo-advisors were not available.

Thanks for that clarification. What’s entailed with managing your own funds?

Is this Tangerine product equivalent to having a financial adviser?

What do you mean by “name brand”?

Very new to this, thanks for any help!

Erin,

Managing your own money is not very difficult, but does require some research. You can basically replicate the Tangerine funds by following the Canadian Couch Potato Strategy.

http://canadiancouchpotato.com/

Tangerine funds are not the same as a financial advisor. Tangerine funds are a form of passive investing which has been a proven strategy that beats 90% of actively managed funds.

If you want to learn more about personal finance, I recommend the Millionaire teacher.

https://www.chapters.indigo.ca/en-ca/books/millionaire-teacher-the-nine-rules/9781119356295-item.html?ikwid=millionaire+teacher&ikwsec=Home&ikwidx=0

My review here

https://www.moneywehave.com/the-millionaire-teacher-review/

As for “Name brand” funds, what I mean is that some people personally trust Tangerine more than a robo-advisor. My personal opinion is that any of the current Canadian robo-advisors including, but not limited to NestWealth, JustWealth, and WealthSimple are all good choices.

“Name Brand” – like a household name – like Kraft Dinner for mac and cheese, or Kleenex for facial tissue. Tangerine does lots of advertising on TV and media billboards.

Barry, am I reading their fees right – if I wanted to start with one of these Tangerine managed investments, and later move to managing on my own to reduce my MER (once I do some more studying up and decide what I want to do), the fee to move the dollars would only be a flat $45?

Hi Andrew,

That is correct. Also that if you’re transferring your funds over, your brokerage may cover that $45 fee so do ask when that time comes.

Don’t take all your funds out, and try to put them with a different broker. You’ll be taxed to death. Be sure to use the appropriate CRA Form (T2033 I think)to move tax-free.

My concern is the conventional wisdom is that to reduce risk simply increase the percentage of your portfolio with Bonds for more safety. With interest rates ‘likely’ to have seen their lows after falling for 35 years what will happen ‘if’ rates have begun a typical reversal trend back up again as history has shown occurs after such a long trend ends. Historically rates rise for 25 to 35 year periods and then reverse. So having a large percentage of Bonds in a portfolio could be like living in an empty bear cave but suddenly finding the bear has come back.This to me is the most important question that needs answering. If so I would like to know what the portfolio managers will do with the Bond portion of your portfolio when they have to maintain your chosen allocation in your fund,especially with those funds mainly in Bonds. Or can they just buy inverse Bond ETFs or short Bonds somehow if Bonds reverse their major trend to down again? Thanks for any insight…………

Ron,

As far as I know, the bond portion of the Tangerine funds simply track a bond index (not sure which one). If the value of bonds fall or rise, they rebalance it by selling our buying some of the equities within the fund.

So if rates have reversed with the trend now up again, Bonds will continue to lose value steadily being that they trade opposite rates. So are you suggesting the fund managers will just continue to sell off equities to maintain the allocation of the selected fund? As they must maintain the allocation of the fund selected. I don’t see how the specific fund with Bonds being a component can’t help but sell off and steadily lose its value as long as Bonds continue to sell off with the trend change. And these Bonds (fixed income) are a major component of investors selecting a safer fund especially those seniors needing safety and reducing risk.

Very informative review, thank you for explaining this subject very clearly for newbies. I currently have about $650,000 in Tangerine Funds (RRSP, TFSA, non registered) and I am at a point where the MERs may be eating up a good chunk of my money. Being 59, not having a pension (except CPP and OAS at 65), this worries. I feel I don’t have the knowledge to invest in TD eSeries ETFs on my own so I have avoided that alternative although it looks attractive. I have recently opened an account with NestWealth, which among robo-advisers would offer the lowest fees for a mid-sized portfolio. My only hesitation: like many, I only trusted brand names -in hindsight a big mistake as I used to have mutual funds with CIBC that never seemed to go anywhere, and I am unsure what it would mean to switch my portfolio to a new kid on the block. What advice would you give me?

Hi Philippe,

You are indeed right that with a portfolio of that size, you’re much better off using ETFs. With NestWealth, it’s run by Randy Cass who’s a former portfolio manager at TD, so it’s not like it’s just some random new person. In addition, your investments in NestWealth are insured up to $1 million by the Canadian Investor Protection Fund (CIPF), so that should give you some peace of mind. Alternatively, you could use a fee only financial planner who has a fiduciary duty to you to help invest / make your money last.

NOTE: That protection is not “protection of los from holding”. It’s loss if NestWealth goes “tits up”

Super info on this sight for every new investor and even older invstors.

Hi Barry!

As you recommended to me above, I read the Millionaire Teacher. Very interesting and accessible. One of his beliefs is that your portfolio should have a percentage allocated to bonds that roughly matches your age. My husband and I are 38 and 40 respectively, so we should have roughly 40% allocated to bonds. Is this a rule you follow?

Based on your review, we opened an investment account with Tangerine and chose the Balanced Portfolio. We’ll probably keep this going for a year or so, but then I’m tempted to move over to the TD e-series. The Millionaire Teacher makes the DIY method sound pretty easy.

Thanks!

Hi Erin,

The Bond rule is a rough guide and it depends on your risk tolerance. I personally use age -10 so in your case, it would be 28 and 30 respectively. However, you also need to consider any other benefits you may have e.g. a defined benefit pension. If you or your husband have a DB pension, you may not need any bonds at all since a DB pension is like a bond.

Going the Tangerine route is a good start. I did that too before I went DIY. TD e-series is great and my wife still uses them. The DIY method is very easy.

Thanks! Another question: If I move over to TD e-series next year, do I have to sell my stocks with Tangerine and re-invest? Or can I transfer them over without selling?

Hi Erin,

Since you’re switching from Tangerine to TD e-series you’re technically selling. That being said, if you’re buying in your RRSP, you can request a transfer in kind. Basically TD would request the transfer from Tangerine. Your funds would then be converted into “cash” while staying within your RRSP (now with TD). You could then allocated to e-series as you see fit. By doing this, you don’t pay tax since all the funds are technically never leaving your RRSP.

If that doesn’t make sense, just send me an email.

If the funds are in a TFSA with Tangerine won’t you not pay taxes still as any interest earned in a TFSA is tax-free? I will be opening a TFSA Investment fund with Tangerine and plan on moving over when I am ready to invest on my own.

Right now I have a very negligible investment account that’s managed with an insurance company. I love the do it yourself mentality however I still have a ways to go learning to do it DIY.

Very glad to have stumbled upon this site. Will be combing through to find more info.

Thanks.

Hi Barbara,

Any interest or capital gains made in your TFSA are tax free. Despite the name “tax free savings account,” you can use your TFSA to house a variety of investments including Tangerine’s investment funds.

Transfer using a CRA Form (T2033 ?????) to avoid being taxed to death.

That makes sense – they stay sheltered. Thanks!

This article and these commens are so helpful and reassuring – thank you!

Two questions:

1. I’ve been advised to invest with someone who has had a long/good standing manager with good performance. I’ve learned that Tangerine’s Silvio Stroescu, Head of Investments had recently left and I’m having trouble finding his successor. Do you know who this may be? Do you think this is cause for caution?

2. Do the Tangerine portfolios automatically reinvest the dividends earned by purchasing additional shares of the fund or so I need to instruct them to do so at the time of purchase?

Thanks!

Hi Noelle,

I don’t know who replaced Silvio, but it’s important to note that past performance is not indicative of future results. Since the Tangerine funds are basically index funds, I don’t think it really matters too much who’s managing things at the top.

The funds do automatically reinvest, there’s no other options so no instructions are needed.

Hi Barry,

1. I understand that the MER fees are lower with passive investing than having your portfolio actively managed. However, if the Tangerine funds or any other funds (such as ETFs) that mimic the index are doing just that – tracking the index – how do you safeguard against a market crash – particularly when you are approaching retirement or have a lower risk tolerance? Are there any studies done on whether actively managed funds are safer than passively managed funds when it comes to volatility and risk (or vice versa)? Never mind the ROI or fund performance when the market is doing well..

2. I also heard that the market is prone to more volatility due to the increase in ETFs and the like b/c (novice) investors are able to move their money around more easily based on their perceptions/emotions. What’s your opinion on that?

Thanks in advance – I appreciate your input!

Hi Esther,

The only thing that can “protect” you from a market crash is by having an asset allocation that is appropriate for your age and risk tolerance. So, if you’re closer to retirement, your portfolio should have more fixed income assets as opposed to equities. on the flip side of things, someone younger should be more heavily invested in equities. It’s not like an advisor can predict when a crash is going to happen. No one can time the markets accurately.

There have indeed been studies and I believe more than 80% of the time, passive investing beats active management. I don’t have the sources available, but the book the Millionaire Teacher does reference findings.

Some analysts believe that due to the popularity of ETFs / passive investing, the markets are skewed, but I personally don’t really believe that. I think it’s a bit silly to think that passive investing is what are actively affecting the markets. I should note that novice investors who are moving their money based on perceptions/emotions are no longer passive investors. They’re active investors who happen to be using passive investments.

Touché regarding the last point! Hmm.. For some reason I always thought the asset allocations + risk tolerance + age had to do with active style of investing only – didn’t realize those were factors to consider for passive investing as well. Thanks for the clarification and for your prompt response!

Hi Barry,

I am new to all of this and have been trying to inform myself.

I have been looking at Tangerine as recommended, however I am a little particular what my money gets invested in. Does Tangerine offer sustainable mutual funds? I don’t want to invest in, oil, pipelines, pesticides or companies that use Child labour. That type of thing k. However the Tangerine investment fund that I was eyeing had Enbridge on their list of mutual funds. Can I request other options? I tried calling them, but I didn’t have 15 minutes to hold to speak to a representative.

CIBC had some nice options, but their MER is 1.8%. I didn’t realize that the MER could make such a substantial difference!

Hi Kathleen,

As these funds track the major indexes, they will be unable to make modifications. You are able to invest in sustainable funds on your own or through an investment advisor, but it will be much more difficult.

Generally speaking, sustainable funds have lagged behind traditional ETFs.

https://www.reuters.com/article/us-usa-funds-sustainableetfs/sustainable-funds-lag-behind-booming-etfs-idUSKCN1B51UR

Copower allows you to invest in green bonds, but bonds should only be part of your overall portfolio.

https://copower.me/en/

Hi Barry,

I am looking into investing and would like to know how to balance this effectively. I am thinking of working with Tangerine as I am new and think that it will provide a good starting point as I continue to learn about the best ways in invest in index funds. My question is that I have a good pension for when I retire so do I need to balance with bonds or could I go with the Equity growth or Dividend portfolios even though I am past 40?

Hi Jordie,

Is your pension a defined benefit pension? If so a good pick would be Equity growth. That being said, it really depends on how much your pension will pay out and what your risk tolerance is. To be honest, it might be better to work with a robo-advisor such as Wealthsimple, Wealthbar, or JustWealth since they can create a custom portfolio based on your profile with a low MER.

Thank you! Yes it is a defined benefit pension. However I will look into the three options you mention here to see what they suggest.

Hi Barry,

I’m looking into investments and doing research as best as I could trying to understand the lingo (which is flying over my head). I’m 25 and working I was curious if opening up a tangerine tfsa investment funds account could be good or if I should open a tfsa/rrsp first would be better? I feel my risk tolerance is medium. Any advice would be much appreciated.

Is it better to invest now or to wait for a drop in markets? Lets say I invest in ING finds now and the market drops, I won’t be able to sell until fund prices (and markets) go well above today’s prices. The only other option will be do invest more when markets are down to avg down.

So should I not wait for markets to come to their senses?

Hi Sam,

What you’re describing is called timing the market. That sounds like a good idea in theory, but the problem is that there’s no way of telling if we’re actually at the top of the markets. A better idea would to simply invest your funds by dollar cost averaging. By dollar cost averaging, you pay the average so hopefully your risk gets reduced.

The saying is, it’s not timing the markets, but time in the market. If your investments are for the long term, I wouldn’t worry too much about current prices. Now if we were talking about buying a house, that would be a different story.

Hi Barry,

I have TFSA investment funds in Balanced at Tangerine. I also want/need to invest more I believe as having it sit in savings is not going to help supplement income in 5 years when I retire without a pension. I do wish to find a CFP but do not want one that works for a bank or investment company from what I am reading. They invest in their own company funds which are all high MER funds which makes no sense to me which is why I have not done anything but sit with what I have in tangerine funds. So with that said, are there any CFP that do not work for an investment company? if so, how do I find one? until then I feel tangerine funds are better than not investing at all.

Hi Lana,

Take a look at the approved list of Financial Advisors from MoneySense.

http://www.moneysenseapproved.com/find-an-advisor/

thank you…..I see that several are in different provinces that come up and also not sure if I want them to purchase investments for me as the fees I am sure will be high…..all overwhelming to me…..

Hi Lana,

If you’re worried about fees and still want a good portfolio, you could work with a robo-advisor such as NestWealth or SmartFolio

Yes I have also been doing some reading on them. I assume there are more options which can possibly mean more opportunity to grow. I understand anything can happen at any time though. Thanks for your suggestions and i will look further into them all.

I opened a Non-Registered Investment Fund Account at Tangerine, my book value is the amount I invested but the my balance is approx. 30$ more. Does that mean I’ve made 30$ in the 2 months its been opened? Also, when do I pay the fees for managing the account? I see no activity on my account so I’m not sure if fees are paid monthly? Yikes, obviously I know so little. Part of the reason I opened this without knowing much is so I could learn as I go. It’s a small amount of money, only 2000$ so that I can I can learn what happens to my money and make good decisions as I go along. That might sound crazy, but I assure you experience is my greatest learning tool. Well that and your advice in this instance 🙂

Hazel,

Book value is what you’ve put in and your balance = markets value. So your portfolio has gone up $30 in value the last 2 months. It’s important to note that this number will change daily and you shouldn’t worry too much about it. Just think long term. Your fees are automatically charged directly to the fund so you wouldn’t physically see that amount deducted.

If you want to learn more, I advise you read the following resources:

https://www.moneywehave.com/index-funds-for-beginners/

http://canadiancouchpotato.com/

Hey thanks so much! I plan on leaving all monies I deposit for about 10 or 15 years. I sincerely appreciate your reply. Cheers Hazel

Thanks Barry, nice review. I worked at Tangerine Investments for over 5 years as an advisor and Trainer of the advisors. It can be a wonderful investment for many who want a managed portfolio. Cheaper does not always equal better, of course. This is the most plain vanilla of the Canadian Robo Advisors. And that might turn out to be a benefit as I outlined in a recent blog.

Having no transaction costs can pay for itself for those who have modest portfolios.

Keep up the great work.

Hey Dale,

Yes, I like the Tangerine funds for their simplicity. They were created before robo-advisers existed which is why they still appeal to so many people.

Thanks Barry, yes it is ironic that they get missed in robo advisor reviews. They were the first Canadian Robo, and they have the greatest assets under management at over $3.5 billion. I would imagine Wealth Simple will catch them within a year or so.

Tangerine is the most plain vanilla of the Robo’s. In turn, they are actually the most Robo of the group. Some of the Robo’s get quite active with the asset allocation.

The funds in all of my Tangerine accounts, where frozen by Tangerine on July 27th, 2018 without warning. The bank issued an emailed a notice to contact them immediately, and a representative told me they had received a Court Order directing them to freeze my accounts, and she provided me with a Court File Number. After almost three months all of my accounts my accounts are still on hold, including Investments and Mutual Funds. Its frustrating dealing with Tangerine, they recently refused to send me a copy of the Court Order, stating that the bank does not send court related documents to clients. After retaining an attorney to handle the litigation we reached a favorable position and I thought my life was getting back on track, but unfortunately my accounts remain frozen. I’m unsure how to proceed and confronting financial hardship, and mounting legal bills. It’s a frustrating situation, I’d gladly take my business elsewhere, if the bank cooperate and release my funds.

I recently heard a program on the radio about doubling up fees with the example of a client who was investing through a portfolio (which had its own mer) but the portfolio owned 14 mutual funds (which had their own respective mers). So, fees were doubled, obviously at the expense of the profit for the client. The portfolio in question made only around 2.5 percent annualized. How can I find out if a tangerine portfolio has a similar make up? I’m not sure I entirely understand the spec sheets for each portfolio….

Hi Wen,

It sounds like the person on the radio was charged for a management fee and then the fees from the MER for the individual funds.

With Tangerine, all their funds charge 1.08%, you pay no additional fees.

Hi Barry,

I’m very new to this and have lots to read to educate myself, but for the beginning I want to try to invest with Tangerine, and learn as I go. I am looking at Balanced growth portfolio. I understand, that transferring your account later on to another institution will come with a $45 penalty. What is Tangerine’s policy of withdrawing, let’s say just the interest acquired, from time to time? Will I be penalized for that? Same question for moving your funds from one portfolio to another one within same institution (Tangerine)?

Thank you for your help.

Hi Natasha,

Things sort of depend on what type of account you set up for your investment funds with Tangerine. FOr example, the $45 fee for moving your account to another financial institution refers to RRSP accounts. If you were to just withdraw the interest acquired, then you’re actually withdrawing from your RRSP which has some pretty big tax consequences as well as permanent loss of RRSP room unless you’re doing for the purpose of the Home Buyers Plan or the Life Long learning Plan.

Let’s say you’re opening the account as a TFSA, then there are no penalties or taxes for removing funds, but note that you need to have the contribution room availabile if you plan on redpositing it back.

For regular taxable accounts, there are no fees for removing cash, but you would pay tax on capital gains.

With Tangerine investment funds, you’re not earning “interest,” you’re hopefully earning capital gains as the investments increase in value. Generally speaking, you only want to invest in these types of funds if your timeline is 5+ years. If you need the money in the next few years, just park your money in a high interest savings account.

If your head is spinning, you may want to consider using a robo-advisor such as JustWealth since you’ll pay fewer fees and you’ll get a bit more support.

https://www.moneywehave.com/justwealth-review/

Hi Barry,

Thank you for your prompt reply.

“With Tangerine investment funds, you’re not earning “interest,” you’re hopefully earning capital gains” – that’s how much I know about investing, so far, but taking baby steps 🙂

I forgot to mention previously that I’m thinking of opening an account as a TFSA. I’m aware of the contribution room and policy for a regular account, I just wasn’t sure about penalties for withdrawing money from an investment account.

I’m an extremely conservative person, so I am already coming out of my comfort zone by planning to invest even a small amount. Thank you for suggesting JustWealth – I’ll be looking into that as well.

Thanks again!

Hey Natasha,

Great that you’re starting to learn about investing. You should look into asset allocation and risk tolerance as those are things that will help you understand investing more. Your timeline matters also. E.g. if you’re 30 years away from retirement, you probably can go with a growth portfolio as long as you don’t panic sell whenever there’s a drop in the markets.

Hi Barry,

First of all, thank you for all your great advice in general and also specifically on Tangerine. I’m 40 years old and currently have a RRSP Mutual funds with TD Bank (under $50k) and a TFSA with Tangerine Balanced portfolio (around $20K). I don’t have much cash flow for auto-invest because I put most of my cash flow towards my employer’s Group RRSP and Shares matching (both at 50% matching so they are guaranteed). My question is: my $50K or so of RRSP sitting in TD Bank is doing pretty much nothing for me, and I’ve not thought about MER/fees before until now. Do you see any valuable in my switching from TD to Tangerine for RRSP/TFSA, knowing that I will likely not invest in either of these due to my cash flow per above.

Thanks in advance for answering my loaded question.

Trevor

Hey Trevor,

Switching your TD RRSP to Tangerine would cut your MER by more than half. If you switched to a robo-advisor, you could lower it a bit more. Considering you still have 25 years until you retire, you might as well switch it to save on the MER.

Also, in the event you ever change employers, you have things set up already.

This may not be relevant, but check the MER on your employer’s gorup RRSP. Although you’re already ahead with the 50% match, if the MER is high, you may want to see if it’s worth transferring it out to wherever you end up moving your personal RRSP once the vesting period has lapsed.

Thanks for your quick reply, Barry. Makes perfect sense. Sunlife has a discounted MER fees for our Group RRSP so i’ll keep my work’s RRSP there during my employment.

My follow-up question, if I may, is if I should switch the type of investment portfolio once I transfer out of TD to Tangerine (or Wealthsimple is the other I’m exploring)? Ie, should I opt the portfolio to something more dividends or income focused since I won’t be putting in much, or does it simply won’t make any difference at all?

Thanks again. I really appreciate your guidance.

Trevor

Hi, I have over $160,000 invested with Tangerine, in 2 Balanced Income Portfolios, RSP and TFSA.

These Portfolios charge the regular 1.07% MER.

I called Tangerine today to inquire about my low (negative) returns.

During the conversation, I realized that, these funds, are 70% bonds and 30% stocks.

During the call, I was told that bonds are paying around 1% in interest.

Therefore, the fees are more than what I make on the 70% that are in Bonds and it is up to the 30% that is invested in the market to carry the complete fees.

Am I wrong on this assumption?

I am 66 years old and retired. I am looking for save income any suggestions?

Also, do you see the bond, GIC rates staying low for the foreseeable future because of the virus, and the growing government debt?

Thanks, A;lex

ALex,

You need to look at the annualized returns over the last few years.

https://www.tangerine.ca/en/products/investing/portfolios/core

In the last 5 years, the return has been 4.88%. When you factor in the MER of 1.07%, your return is 3.81. Which this is nothing special, it is in line with what the expected returns for a portfolio with 70% fixed income.

I’m not sure what you mean by saving income. This portfolio is very conservative and appropriate for someone of your age.

Bond ladders would be even safer, but would likely yield a lower return.