How to Read a Credit Card Statement

Knowing how to read a credit card statement is basic financial literacy, but it can be confusing if you’re getting a credit card for the first time or you’ve recently switched banks. To further complicate things, if you have a points or cash back credit card, every financial institution uses a different way to show the rewards you’ve earned for the previous billing cycle.

Once you understand how to read a credit card statement, you can make smarter financial decisions. That’s because you’ll be able to see what purchases you’ve made, how much credit you’ve used, and how many rewards you’ve earned. Here’s how to read a credit card statement.

What is a credit card statement?

First off, a credit card statement is a paper or digital statement that lists all of the transactions charged or refunded to your credit during the previous billing cycle. This would include things such as purchases, pre-authorized purchases, annual fees, and refunds.

Billing cycles typically last one month, and you get a minimum of 21 interest-free days. As long as you pay your entire balance on time, by the statement due date, you will not incur any interest charges.

Every credit card statement will include the following information:

- Credit card – Right at the top of the credit card statement, you’ll see which credit card the statement is for and your name. This is vital information if you have multiple credit cards with the same bank.

- Your name and credit card number – Below the credit card name, your statement will display your name and credit card number. Note that for privacy reasons, some of the digits of your credit card will be blocked out.

- Statement date – This is the date that your statement was issued.

- Statement period – The credit card statement period refers to the time period where your transactions would apply.

- Transactions – Under transactions, you’ll see a few different items. The transaction date is when you made the purchase. The post date is when the charge officially appeared as a charge on your credit card. Activity description usually refers to the name of the merchant where you made the purchase. Finally, you’ll see the amount due.

- Total new balance – The credit card statement balance is how much you owe. If the number is in the negatives, that means you have an outstanding credit.

- Contact information – The contact numbers for your financial institution and loyalty program (if applicable) would appear here.

- Points/cash back earned – For those that have a points or cash back credit card, this section would show you what you’ve earned during the statement.

- Payment information – Arguably the most important section, the payment information, or account summary, displays your payment due date, credit limit available credit, and the annual interest rate for purchases and cash advances.

- Estimated time to pay – This calculation shows you how long it would take to pay your total balance if you only made the minimum payment each month.

- Calculating your balance – Under this final section, it would list any additional fees that would apply for the month, such as balance transfers, cash advances, interest, and late fees.

- Payment details – At the bottom of your statement, is a detachable portion that lists your payment details. This would be used if you pay at a branch or by mail.

Credit card statement example

The next step to learning about how to read a credit card statement is to look at a credit card statement example.

As you can see, this is from my TD Aeroplan Visa Infinite Privilege Card. The sections I always check are transactions and Aeroplan points earned.

How often do credit card statements come?

Your next natural question might be how often do credit card statements come. They’re sent once a month immediately after your billing period ends. If you opt for paperless statements, they’ll be sent to your online banking account. Note that you’ll get an email alert when your statement is ready. For those that opt for physical statements, you can expect them in your mailbox a few days after your statement date.

While paper statements are convenient, some financial institutions may give you an incentive to go paperless. For example, you might get bonus points or cash back.

Your statement date would usually line up with the time you signed up and were approved for the account. For example, say you signed up on the 17th of the month. Your statement date would typically fall on the 17th of every month. You could request a different statement debt. You’d just have to call your credit card provider.

What to check for on your credit card statement

When learning about how to read a credit card statement, you need to check for a few specific things every month:

- Suspicious transactions – Check your credit card statement and review every line in the transactions section. What you’re looking for is any purchase you don’t recognize. If something looks off, investigate further by looking up the merchant that charged you. If you’re positive the purchase wasn’t made by you, contact your financial institution to start a fraud claim.

- Interest and fees – Anyone that pays their bills on time and in full should check the interest and fees under the calculating your balance section. You want to make sure no additional charges, such as balance protection, were added.

- Credit card balance – Since this is the amount you owe, you need to know what it is so you can make a payment.

How points and cash back are calculated on credit card statements

If you earn points or cash back with your credit card, you’ll want to pay close attention to the breakdown. With cash back credit cards, the calculation is quite simple since it’s based entirely on your earn rate.

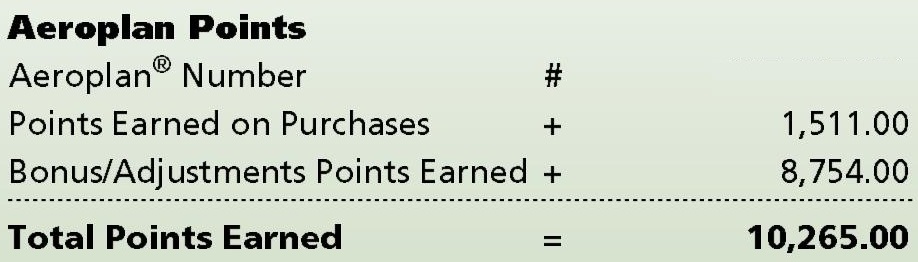

However, with points cards, it’s not always so easy to understand the breakdown of your points. Let’s use my TD Aeroplan Visa Infinite Privilege credit card statement as an example again, but note that every reward program is different.

As you can see, there are points earned on purchases and bonus/adjustment points earned. This should be a simple calculation, but TD/Aeroplan makes it a bit more complicated than it needs to be. For points earned, the points earned refer to the base earn rate of 1.25 Aeroplan points per $1 spent. However, you earn 1.5 points per $1 spent on eligible gas, groceries, travel and dining purchases. The extra .25 points appear under bonus/adjustment points earned. Any bonus points, such as promotions, would also fall under bonus/adjustment points earned. For this statement, I received an extra 5,000 Aeroplan points when spending $1,000.