DIY Investing: Is it right for you?

Whether you’re a novice or an experienced investor, you hope that you can reach your financial goals by investing in the stock market. Perhaps, along the way, you’ve wondered whether you have what it takes to go the DIY (do-it-yourself) route. Before you make that decision, I’ll compare your options so you know what you’re getting yourself into. Then, I’ll show you how easy it is to make the switch to become a DIY investor.

This is a first article of a six-part DIY Investing series, which will span over the course of a few months. As a self-directed investor for a dozen years, I’ll be sharing some of my experience and expertise to guide you to become a DIY investor.

Why you should invest in the stock market

If you haven’t already started investing in the stock market, there are plenty of reasons why you should start now. If you have some money that you’ve saved up that’s sitting in a low-interest savings account that you don’t need to touch anytime soon (and you’ve got your emergency fund topped up), then you may benefit from investing it. That way, you can earn interest on your money and it will help you reach your financial goals much faster through compound interest and dividend payouts.

Before you start investing, it’s important to think about what your financial goals are. Perhaps you are looking to save for retirement, achieve financial independence/retire early (FI/RE), quit your full-time job, or start a family. Whatever your reason, investing your money is a great way to have money work for you and to grow your net worth.

3 ways to invest your money in the stock market

Here I’ll explain the three common options for you to start investing your money.

Using a financial advisor

If you’ve received an inheritance, windfall, or have a complex financial situation, going with a financial advisor may be helpful. They can sit down with you and provide advice on how to invest your money. However, be sure to check if they are tied to specific institutions or products and they should disclose upfront what their fees are. A fee-only advisor can be a good option if you want unbiased advice.

Since it’s not an entirely regulated industry yet (anyone can give themselves a fancy title to sound legit), you’ll want to check that they have the proper credentials and can suit your needs. Since they make a living from fees, they typically only work with high net worth clients ($250K to $1M+) and their fees can be quite high. Ask for recommendations, referrals and interview several candidates before you make a decision.

Going with a robo advisor

With as little as $1,000, you can start investing with a robo-advisor. Typically you’ll fill out a questionnaire and an algorithm will assemble your portfolio. The fees are in the middle of the road: you’ll still need to pay the management expense ratios (MER) of the funds you buy and the cost of having a robo-advisor manage your portfolio for you. For some high-net worth investors, the provider may offer services of a human advisor. This option is a good choice for those who want to be more hands-off with their investments but don’t want to pay high fees with a financial advisor.

DIY investing

Becoming a self-directed investor can be a suitable choice for individuals who feel like they have good investing knowledge and want to have full control over which funds they hold in their portfolio and save on fees. Since you’re responsible for your performance, it’s important to keep your emotions out of the equation so that you don’t start tinkering with your portfolio. Your success will be based on your own decision-making ability.

If you’re looking for a discount brokerage where you can start investing with low fees, consider opening a Qtrade Direct Investing account where you can get up to $150 in bonus cash.

What is compound interest?

Remember when you were a kid and you built a huge snowball? At first, it takes a lot of effort to get the ball going, but once it gets bigger, it gets easier to roll. That’s the same way compound interest works in the stock market.

When you first start investing with a small amount of money, you’ll see your account grow slowly. Then the pace picks up and the money will accumulate at a faster rate over the long term.

In this chart below, you can see that if you were to invest $6,500 a year (the current annual TFSA contribution limit) with an annual interest rate of 6%, after 10 years it will be worth $85,675.17 when compounded yearly. Even though your total investment will be $65,000, you will have earned $20,675.17 in compounded interest. That’s why Warren Buffett called “compounding interest the 8th wonder of the world.”

| Year | Total investment | Yearly interest | total interst | Total value |

|---|---|---|---|---|

| 1 | $6,500 | $0 | $0 | $6,500 |

| 2 | $13,000 | $390 | $390 | $13,390 |

| 3 | $19,500 | $803.40 | $1,193.40 | $20,693.40 |

| 4 | $26,000 | $1,241.60 | $2,435 | $28,435 |

| 5 | $32,500 | $1,706.10 | $4,141.10 | $36,641.10 |

| 6 | $39,000 | $2,198.47 | $6,339.57 | $45,339.57 |

| 7 | $45,500 | $2,720.37 | $9,050.94 | $54,559.94 |

| 8 | $52,000 | $3,273.60 | $12,333.54 | $64,333.54 |

| 9 | $58,500 | $3,860.01 | $16,193.55 | $74,693.55 |

| 10 | $65,000 | $4,481.62 | $20,675.17 | $85,675.17 |

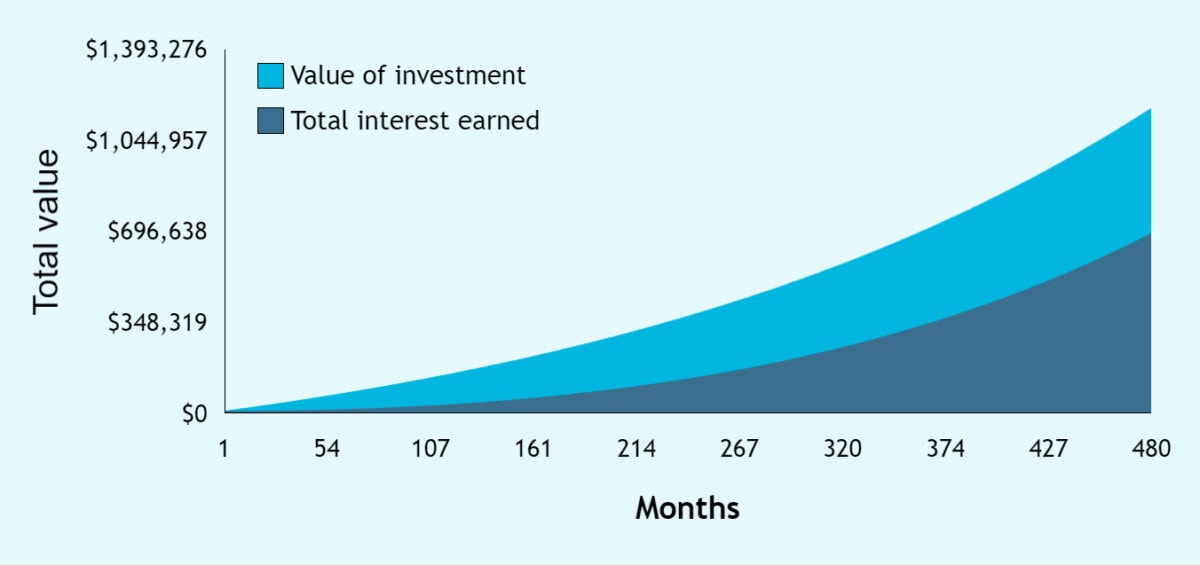

How compound interest can help you grow your portfolio

Here’s a comparison chart showing how much your investment will grow annually, based on a certain monthly contribution and a certain annual interest rate.

Please note: the following is for illustrative purposes only. There is no guarantee when it comes to investing as there are always risks involved.

| Amount per month | 40 years @ 4% interest | 40 years @ 6% interest | 40 years @ 8% interest |

|---|---|---|---|

| $100 | $116,106.38 | $190,767.78 | $322,107.93 |

| $500 | $580,531.88 | $953,838.88 | $1,610,539.67 |

| $1,000 | $1,161,063.76 | $1,907,677.76 | $3,221,079.35 |

In the diagram above, if you had a monthly investment of $100.00 at an annualized interest rate of 4% will be worth $116K after 40 years when compounded yearly.

Bumping this up to $500 per month, at a 6% interest rate, your investment will be worth $953K.

For the super savers, if you invested $1,000 per month, at a 8% interest rate, you’ll have a jaw-dropping net worth of around $3.2 million after 40 years.

You can use this compound interest calculator and plug in your numbers to see how much your investments can grow. This goes to show that the longer your time horizon (the amount of time you have to invest your money), then the more time for compounding interest to work its magic!

The benefits of switching to DIY investing

As humans, it can be easy to sit on the fence and not make any changes. However, as I’ve illustrated above how much money you’re wasting on excessive fees, may be the tipping point for some of you to make the decision to become a self-directed investor. Plus, if you want to be in the driver’s seat to select your funds, then it’s a good reason to hop over the fence.

When I decided to switch my mutual funds from one of the big banks over to an online brokerage, all it took was a few hours of my time filling out some paperwork, and mailing it in. Again, that was over a decade ago and technology has made it a lot faster and easier.

Nowadays, you can fill out the paperwork online to expedite the processing times. Once you open an account with your new online brokerage, you’ll be able to transfer your money from your existing RRSP and/or TFSA.

There are several ways to bring your money over. The most common method when you fill out the transfer form, is to checkmark the box to transfer in-kind so that it ports everything as-is to your new brokerage. It may take a few weeks, so you’ll have to be patient. Once this is complete, you’ll be able to start managing your investment portfolio and save on fees immediately.

Make the switch and get started

There are many benefits when it comes to DIY investing such as minimizing your fees and being in control of your investment decisions. For those of you who are making the switch from a financial advisor or robo advisor to an online brokerage, then you’ve got your work cut out for you. If you’re willing to make the commitment to learn (which is why you’re here reading this!), then soon you’ll be able to reap the benefits of becoming a self-directed investor.

Remember, you don’t need to know everything about investing—just the basics to get you started.

You’ll always have the opportunity to make adjustments as you become a more experienced investor. Unlike a decade ago, there are so many options available to you. The key is to get started early so that you can take advantage of compound interest.

The next part of this DIY Investing series focuses on learning about your investor personality type.